Are Pensions Still Tax-Efficient? The 2027 changes to pension tax.

Today, we’re diving into a topic that’s not only important but also a bit of a game-changer for anyone planning their financial legacy

Here’s the headline, one we’ve heard a lot since the budget announcement in October 2024: Pensions will be subject to inheritance tax from 2027. This is a major shift from the current rules, where pensions can often be passed on free of IHT.

So, what does this mean for you, your family, and your estate planning? Is your pension still the golden goose of tax efficiency, or is it time to rethink your strategy?

To break it all down, we’re going to walk you through a case study. We’ll take a look at how this new rule could impact John and Angela, a couple with a £900,000 estate, and what their beneficiaries might face under different scenarios.

But before we get into the ins and outs, let’s set the stage. Estate planning can feel overwhelming, especially with all the jargon and rules. That’s why we’re here: to make it simple, clear, and actionable. So, let’s unravel the mystery of IHT and the new tax rules could affect your pension.

Overview of Inheritance Tax on pensions and ISAs

First, let’s quickly review the basics of inheritance tax, or IHT. In the UK, IHT is charged at 40% on the value of an estate above the nil-rate band (NRB). Currently, the NRB is set at £325,000 per person, with an additional residence nil-rate band available in certain circumstances. Traditionally, pensions have been seen as a tax-efficient way to pass on wealth since they can currently be passed on free of IHT. However, starting in 2027, pensions will also be subject to IHT, significantly changing their role in estate planning.

It’s important to note that if the owner of a pension dies before the age of 75, the beneficiary can access the pension without incurring income tax. If the donor dies after the age of 75, the beneficiary must pay income tax at their marginal rate on any withdrawals.

ISAs, on the other hand, are subject to IHT but do not incur additional income tax for beneficiaries. To illustrate the impact of these changes, we’ll examine a case study involving John and Angela’s estate. Their £900,000 estate is split between pensions and ISAs, and we’ll analyse three scenarios to determine how much IHT and income tax their son, Adam, a basic rate taxpayer, will pay.

Inheritance tax on pensions and ISAs: John & Angela

Here’s the scenario: John and Angela are a married couple with a £900,000 estate comprised entirely of pensions and ISAs. John passes away first, leaving everything to Angela, which is tax-free due to the spousal exemption. Angela later passes away after the age of 75, in May 2027, when pensions will also be subject to IHT. The entire estate is left to their son, Adam.

As John left everything to Angela, his Nil Rate band is retained in full. The executors of the estate are therefore able to use both Angela’s and Johns Nil Rate band to reduce the value liable to IHT, a combined value of £650,000.

We’ll explore three scenarios where the estate is divided differently between pensions and ISAs. Assuming Adam withdraws the full value of the inherited pension over a number of years, keeping his income tax rate at 20% throughout, we’ll calculate the IHT and income tax liabilities in each case. Let’s start with the first scenario.

Scenario 1

In the first scenario, the estate is evenly split between pensions and ISAs, with £450,000 allocated to each. Let’s take a look at the numbers and see the IHT due and Adams income tax liability:

The ISA portion of £450,000 is subject to IHT after applying the £325,000 NRB. This leaves £125,000 subject to IHT, resulting in an IHT bill of £50,000.

The pension portion of £450,000 is also subject to IHT. After applying the same £325,000 NRB (shared across both pensions and ISAs), another £125,000 is subject to IHT, resulting in an additional £50,000 IHT bill.

As Angela died after age 75, Adam will pay income tax on drawings from his late mother’s pension. As a basic rate taxpayer, Adam will pay 20% income tax on these withdrawals, amounting to £80,000.

The total tax liability in this scenario is £180,000.

This leaves Adam with net proceeds of £720,000 from the £900,000 estate.

Scenario 2

In the second scenario, John and Angela preserved the value of their pensions prior to their death, assuming this would be a more tax efficient approach. As a result, the estate is weighted more heavily toward pensions, with £600,000 in pensions and £300,000 in ISAs. Note in this scenario that the available Nil Rate Band is applied proportionately to the ISA and pension accounts, based on their value. Here’s what happens:

The ISA portion of £300,000 is subject to IHT after applying the proportionate NRB of £216,667. This leaves £83,333 subject to IHT, resulting in an IHT bill of £33,333.

The pension portion of £600,000 is subject to IHT after applying the remaining NRB of £433,333. This leaves £166,667 subject to IHT, resulting in an IHT bill of £66,667.

After the deduction of IHT, Adam will also pay 20% income tax on the £533,333 pension withdrawals, which amounts to £106,667.

The total tax liability in this scenario is £206,667.

Adam’s net proceeds in this scenario are £693,333.

Scenario 3

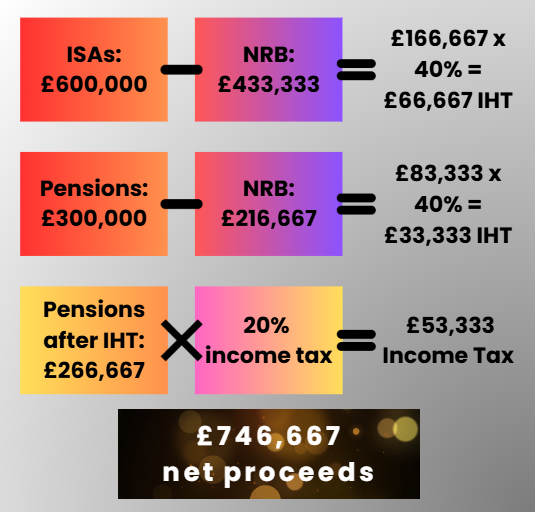

Finally, in the third scenario, John and Angela were forewarned about the changes in pension taxation. As a result, the estate is weighted more heavily toward ISAs, with £600,000 in ISAs and £300,000 in pensions. Let’s look at the outcome:

The ISA portion of £600,000 is subject to IHT after applying the proportionate NRB of £433,333. This leaves £166,667 subject to IHT, resulting in an IHT bill of £66,667.

The pension portion of £300,000 is subject to IHT after applying the remaining NRB of £216,667. This leaves £83,333 subject to IHT, resulting in an IHT bill of £33,333.

Adam will also pay 20% income tax on pension withdrawals, amounting to £53,333.

The total tax liability in this scenario is £153,333.

In this scenario, Adam’s net proceeds are £746,667.

Case study take away

When we compare the three scenarios, it’s clear that the way the estate is divided between pensions and ISAs has a significant impact on the total tax liability and the net amount Adam receives. Here’s a quick recap:

Scenario 1 (Equal Split): Net proceeds of £720,000.

With an equal split in pensions and ISAs, the net proceeds of the estate, following a full withdrawal from the pension, amounts to £720,000.

Scenario 2 (More Pensions): Net proceeds of £693,333.

With a greater weighting to pensions, the net proceeds are lower by £26,667, with an amount of £693,333 received.

Scenario 3 (More ISAs): Net proceeds of £746,667.

Finally, with a greater weighting to ISAs, the total net proceeds are the highest out of the three scenarios, with an amount of £746,667 received.

From these results, we can see that the upcoming changes to pension taxation in 2027 make ISAs relatively more attractive for inheritance planning in these scenarios. While pensions still offer tax benefits, the inclusion of IHT reduces their overall efficiency for passing on wealth.

Final Thoughts

So, what’s the key takeaway? With pensions becoming subject to IHT from 2027, it’s essential to reconsider how you structure your estate. Balancing your assets between ISAs and pensions could help minimize the overall tax burden for your beneficiaries. Pensions have long been thought of as the gold standard for passing wealth on tax efficiently. Depending on your circumstances, this still may be the case, however from 2027 pension holders will be looking at these wrappers in a different light.

Get in touch

Do you have a question about estate planning? We’re here to make it simple. Leave us a message via the submission form button below, and let’s chat. We’re always happy to help.

No financial decisions should be taken based on the content of this website or associated videos. The guidance contained within this website is subject to the UK regulatory regime and is therefore primarily aimed at viewers in the UK. Always take full individual advice first. Regulations and legislation governing taxation, investments and pensions may change in the future.

The content on this page is accurate as of the 2024-25 tax year.