A Guide to Annuities

Let's talk about something that's making a big return in retirement planning: annuities. You might have heard the term before, perhaps even dismissed it as a bit old-fashioned. But under current market conditions, annuities are becoming an increasingly attractive option for securing a reliable income in retirement, especially here in the UK.

This resurgence is clearly reflected in recent figures: in 2024, UK annuity sales experienced a significant increase, with a 24% rise in the number of contracts sold and a 34% increase in total sales value compared to 2023, marking a new ten-year high for annuity sales, reaching £7 billion.

We'll break down the different types, explain the crucial link between gilt yields and annuity rates, and even show you how inflation plays a fascinating role in your annuity income rates.

What Exactly Is An Annuity and Why Should Retirees Care?

In simple terms, an annuity is a financial product that you purchase, usually with a lump sum of money from your pension pot, in exchange for a guaranteed income for the rest of your life, or for a set period. Think of it as exchanging a chunk of your savings for a regular, predictable salary in retirement.

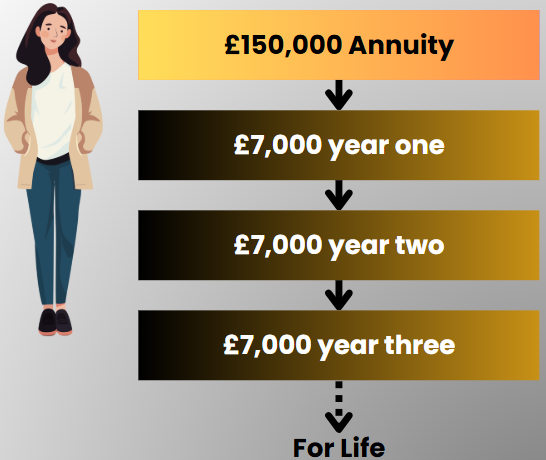

Let's imagine Sarah, aged 65, has a pension pot of £150,000. She's worried about market volatility and wants a secure income for life. She could use £150,000 to purchase an annuity. Let's say, for simplicity, this buys her an income of £7,000 per year for the rest of her life. Sarah now knows that no matter what happens, she has that £7,000 coming in every year. This certainty allows her to plan her retirement spending with confidence.

Now, why should retirees care? Well, for many, the biggest worry in retirement is outliving their savings – the fear of running out of money. This is where annuities truly shine. They offer:

Guaranteed Income: This is the big one. Unlike drawing down from your pension pot where you manage the investments and the withdrawals yourself, an annuity removes that investment risk. You know exactly how much income you'll receive, come rain or shine, market crash or boom. This provides incredible peace of mind.

Longevity Protection: With people living longer, annuities provide a safeguard against the risk of living beyond your expected lifespan. No matter how long you live, your annuity income continues.

Simplicity: Once you've set it up, an annuity is relatively hands-off. You don't need to worry about managing investments or making withdrawal decisions. The income simply arrives in your bank account.

Different Types of Annuities (A Non-Exhaustive List)

Annuities aren't a one-size-fits-all product. There are different types designed to meet varying needs and preferences. Understanding these differences is key to choosing the right option for you. Let's break down the main ones:

Level Annuity: This is the most straightforward type. You receive a fixed income that stays the same for the entire duration of the annuity, whether that's for life or a set period.

The benefit here is predictability. You know exactly what you're getting each year. However, the downside is that inflation will erode the purchasing power of your income over time. What feels like a good income today might buy you less in 10 or 20 years.

RPI Annuity (Retail Price Index Linked): This type of annuity aims to combat the effects of inflation. Your income will increase each year in line with the Retail Price Index (RPI), which is a common measure of inflation in the UK.

This offers greater long-term purchasing power. However, because the insurer is taking on the inflation risk, the initial income you receive from an RPI annuity will be *lower than that of a level annuity for the same premium. It’s a trade-off: lower starting income for future inflation protection.

LPI Annuity (Limited Price Indexation Linked): Similar to RPI annuities, LPI annuities also provide inflation protection, but with a cap on the annual increase. This cap is often set at a specific percentage, for example, 3% or 5%.

LPI annuities offer a middle ground. They provide some protection against inflation, but the cap means that if inflation skyrockets, your income won't keep pace fully. Because of the cap, the initial income offered will typically be higher than an RPI annuity but lower than a level annuity.

Short-Term Annuity: Unlike the 'for life' annuities, a short-term annuity pays an income for a fixed period, typically between 5 and 10 years. After this period, your pension pot is not exhausted, and you would need to decide what to do with the remaining funds – perhaps purchase another annuity, go into drawdown, or take it as a lump sum.

These can be useful for those who want a guaranteed income for a specific period, perhaps to bridge a gap until your state pension kicks in, or if you are unsure about your long-term plans. They offer flexibility, but you need to be mindful of what happens at the end of the term.

The choice between these types depends on your priorities. Do you value a higher initial income and are comfortable with the risk of inflation eroding its value over time? Or do you prefer a lower starting income but with the security of inflation protection?

Gilt Yields and Annuities

Now, let's talk about something crucial that's been driving the recent resurgence in annuity popularity: gilt yield rates. You might be asking yourself “What are gilt yields and what do they have to do with my retirement?" Well, surprisingly, they have a significant impact on what you can expect from an annuity.

Gilt yields are essentially the interest rates on UK government bonds – what the government pays to borrow money. When gilt yields rise, annuity rates tend to rise too. Why? Because annuity providers invest the money you pay for your annuity into assets like gilts to generate the income they promise to pay you.

When gilt yields are high, insurers can generate a better return on their investments, meaning they can offer you a more attractive income for your money. Conversely, when gilt yields are low, annuity rates tend to be lower.

We've seen a significant increase in gilt yields over the past year or so, largely due to rising interest rates as the Bank of England tackles inflation. This is fantastic news for anyone considering an annuity.

This direct correlation is why annuities are looking so much more appealing right now. If you're nearing retirement, or even if you're a few years away, keeping an eye on gilt yields is a smart move. Higher yields often translate into more generous annuity offers.

Level Annuities Vs. Indexed Annuities

This is where it gets really interesting when comparing level annuities with inflation-linked annuities. On a like-for-like premium basis, a level annuity will (almost) always provide a higher starting income than an inflation-linked annuity (like RPI or LPI). This makes sense, as the insurer isn't taking on the risk of future inflation increases with a level annuity.

However, the magic of compounding and inflation comes into play with indexed annuities. While your initial income is lower, it increases each year. Over time, that cumulative increase means that at a certain point in the future, the income from your indexed annuity will overtake the income from a level annuity, and continue to grow, providing you with greater purchasing power.

Let's illustrate this with an example:

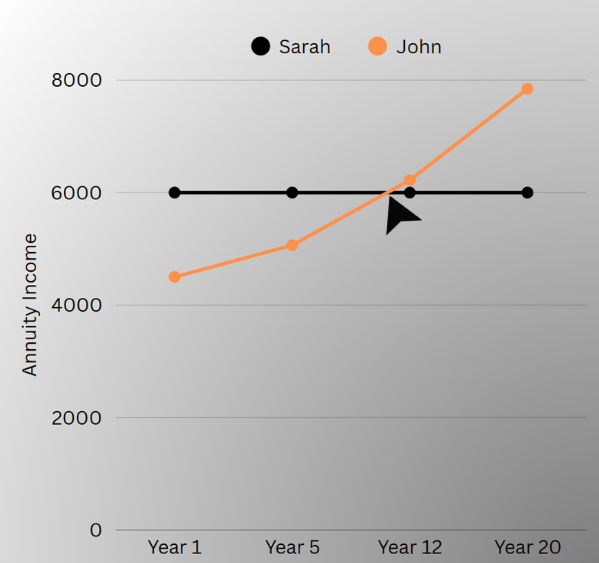

In this scenario, Sarah, aged 65, decides to go with Option A, the Level Annuity, receiving £6,000 per year. Her friend John, also 65, goes with Option B, the RPI Annuity, initially receiving £4,500 per year.

Let's assume an average inflation rate of 3% per year.

In Year 1: Sarah receives £6,000. John receives £4,500.

In Year 5: Sarah still gets £6,000. John's income has increased to approximately £5,065.

In Year 12: Sarah is on £6,000. John's income has now reached approximately £6,220. At this point, John's annual income has now overtaken Sarah's.

In Year 20: Sarah's income is still £6,000. John's has surged to approximately £7,845. His income is now significantly higher and continues to grow, providing greater purchasing power.

This crossover point is crucial. For John, even though he started with less, his income began to provide more purchasing power in the long run.

The real game-changer is this: The higher the inflation rate, the earlier that crossover point will be achieved.

If inflation were to average 5% instead of 3%, John's income would grow even faster, and he'd overtake Sarah's level income at an even younger age. This is why, in periods of higher inflation, indexed annuities become even more compelling. They offer a powerful antidote to the erosion of your purchasing power over time.

While the immediate gratification of a higher initial income from a level annuity is tempting, for those with a longer life expectancy or a greater concern about future living costs, an indexed annuity can prove to be a much more financially robust option in the long run.

Are Annuities Right For You?

So, we've explored what annuities are, their different types, and how market conditions like gilt yields and inflation impact their attractiveness. But the big question remains: are they right for you?

Annuities offer undeniable benefits like guaranteed income and longevity protection, which can be invaluable for peace of mind in retirement. However, they also come with some trade-offs and considerations:

Loss of Flexibility: Once you buy an annuity, your money is locked in. You can't usually get access to the lump sum again.

No Investment Growth (Typically): Unlike pension drawdown, your money isn't invested in the market, so you won't benefit from potential investment growth.

Inheritance: Depending on the type of annuity, there might be limited or no lump sum to pass on to your beneficiaries after you pass away. However, you can add features like a 'guarantee period' or 'value protection' to an annuity to ensure some capital is paid out if you die early.

So, who might an annuity be particularly suitable for?

Individuals who prioritise guaranteed income and security above all else.

Those who are risk-averse and don't want to manage investment decisions in retirement.

People with a longer life expectancy who want protection against outliving their savings.

Anyone looking to cover essential living costs with a reliable income stream.

The annuity market is complex, and rates can vary significantly between providers. It's crucial to:

Shop Around: Don't just accept the first offer you receive. Use an annuity broker or comparison service to get quotes from multiple providers.

Consider Your Health: If you have any health conditions or are a smoker, you might be eligible for an enhanced annuity, which could provide a higher income. Be sure to disclose all relevant health information.

Seek Financial Advice: This is perhaps the most important step. A qualified financial advisor can assess your individual circumstances, explain all your options (including drawdown and a combination of both), and help you make an informed decision that aligns with your retirement goals.

Final Thoughts

Annuities, often overlooked in the past, are experiencing a renaissance. The current high gilt yields are making them a genuinely attractive option for securing a guaranteed income in retirement. While they offer predictability and protection, it's vital to understand the different types, the impact of inflation, and whether their characteristics align with your personal retirement strategy.

Remember, your retirement is unique, and so too should be your financial plan. Take the time to understand all your options, get professional advice, and make the choice that gives you the peace of mind and financial security you deserve.

Get in touch

Do you have a question about retirement planning? We’re here to make it simple. Leave us a message via the submission form button below, and let’s chat. We’re always happy to help.

No financial decisions should be taken based on the content of this website or associated videos. The guidance contained within this website is subject to the UK regulatory regime and is therefore primarily aimed at viewers in the UK. Always take full individual advice first. Regulations and legislation governing taxation, investments and pensions may change in the future.

The content on this page is accurate as of the 2025-26 tax year.